MongoDB Company Snapshot

Products & Services: MongoDB (ticker: MDB) powers modern applications with its document‑oriented database engine. Its Atlas platform delivers a fully managed, global cloud service that seamlessly scales schema‑flexible workloads.

Revenue Model: A subscription framework combining Atlas and enterprise support that drives predictable, recurring revenue and expanding margins.

Customer Success: For example, Expedia relies on Atlas to manage real‑time booking data at peak scale. Because travel data can change constantly: different destinations, itineraries and user preferences, a flexible document model and automatic horizontal scaling let Expedia adapt instantly to shifting travel patterns and traffic spikes without negatively impacting customer experience.

💡 MongoDB benefits by not having a clear competitor: Microsoft Cosmos DB, Amazon DynamoDB, Databricks document store and Oracle’s JSON engine all miss the mark with rigid models or limited developer experience and ecosystem.

A Key Financial Move Behind MongoDB’s Growth Story

MongoDB surged to roughly $445/share in early 2024 on sky‑high growth expectations, but its late‑2024 decision to convert over $1 billion of debt into equity sent the stock tumbling to about $160/share as outstanding shares nearly doubled. Far from signaling a breakdown in fundamentals, this move wiped away a massive debt burden and shored up financial flexibility, transforming MongoDB into a debt‑free, cloud‑native growth engine.

💡 MongoDB converted its lenders into equity stakeholders: aligning their interests with the company’s success, eliminating fixed interest obligations, and ending future debt rollover cycles.

With Atlas adoption still accelerating and a cleaner capital structure in place, today’s drawdown represents an attractive entry point for investors aiming to ride the next leg of its runway toward a $400 target by end of 2026.

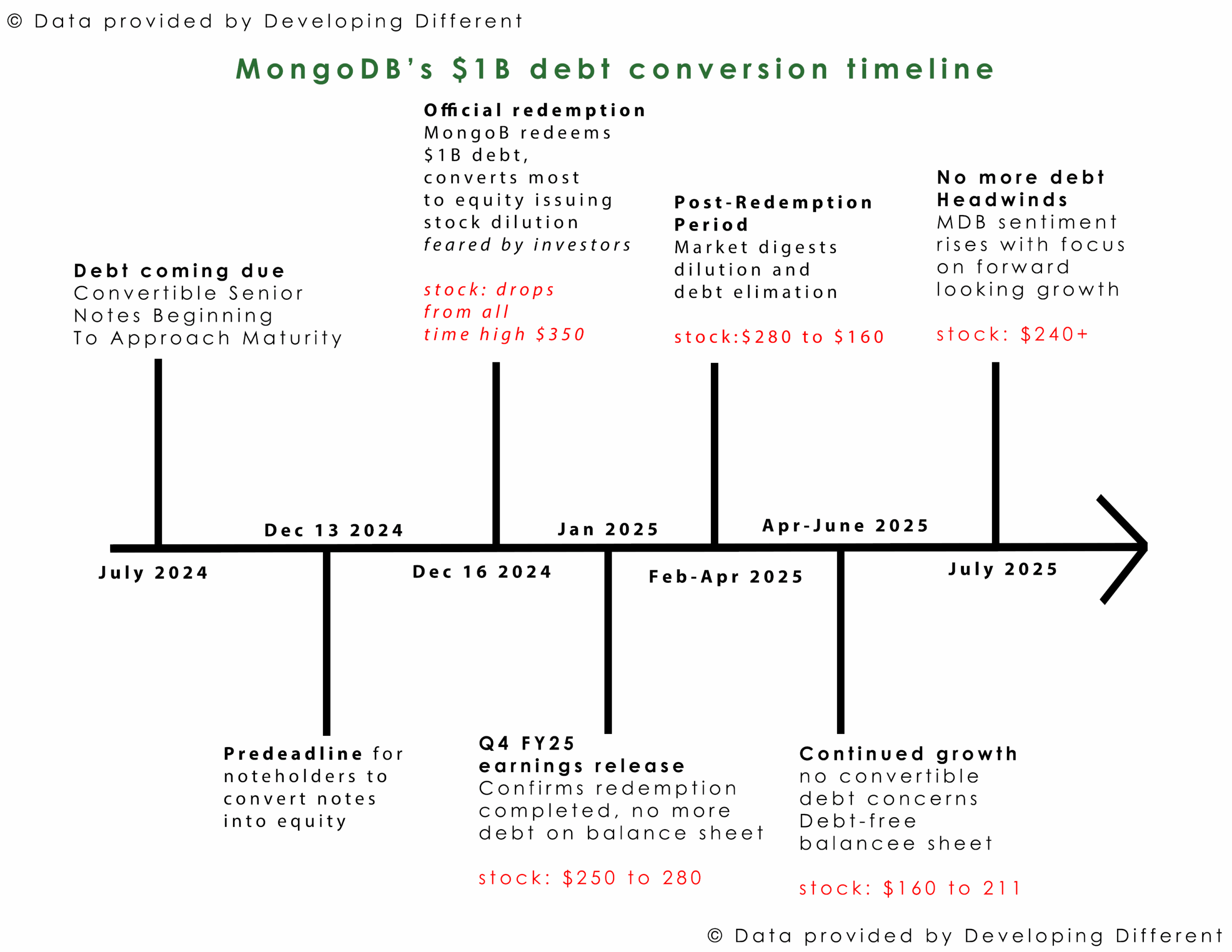

What MDB’s $1B Debt Redemption Means for Investors

MongoDB redeemed all of its 2026 Convertible Notes on December 16, 2024 (Q4 FY 2025), eliminating over $1 billion in debt. Converting that debt into equity injected a substantial number of new shares into the market, diluting existing shareholders. As investors digested the improved balance sheet, the share price initially declined before stabilizing.

Key Benefits

- Strengthens the company’s financial position by removing near‑term obligations

- Improves leverage ratios and credit profile

- Reinforces investor confidence in long‑term profitability

Key Considerations

- Future earnings per share will adjust to reflect the larger share base

- Equity dilution may exert downward pressure on the share price in the short term

Debt Redemption and Balance Sheet Impact

Below is a summary of MongoDB’s quarterly balance sheet changes around the debt redemption. In Q4 FY 2025, $1.72 billion of debt was reduced to $648 million by issuing additional equity, increasing shareholders’ equity from $1.61 billion to $2.78 billion.

View MDB SEC filings ↗| Quarter | Q2 FY25 (Jul 2024) | Q3 FY25 (Oct 2024) | Q4 FY25 (Jan 31, 2025) | Q1 FY26 (Apr 30, 2025) | Q2 FY261 (Aug 28, 2025) |

|---|---|---|---|---|---|

| Total Assets | $3.27B | $3.33B | $3.43B | $3.62B | $3.75B |

| Cash & Short-Term Investments | $2.15B | $2.22B | $2.30B | $2.45B | $2.55B |

| Total Liabilities | $1.77B | $1.72B | $648M ▼ | $591M | $585M |

| Total Debt | $80M | $78M | $74M | $72M | $70M |

| Shareholders’ Equity | $1.50B | $1.61B | $2.78B ▲ | $3.03B | $3.17B |

| Share Price | $250 to 230 | $270 to 330 | $250 to 280 | $170 to 190 | Upcoming |

- Q2 FY26 aligns with MDB guidance ↩︎

💡 Developing Different insight: an informed investor combing through MongoDB’s financials would have spotted the short-term mounting debt load well before the conversion, anticipating that swapping over $1 billion of debt for equity would double the share count, thereby halving the stock price, before ultimately laying the groundwork for stronger, debt‑free growth.

Review the debt timeline below to see how this would play out on the stock price in the real world market:

The stock essentially cratered in half, going from all time high $360/share to $160/share. But, this drop didn’t happen in January when the conversion redemption completed, it took till February for the decline to start and April for it to hit bottom.

💡 Given that investors were alerted to the impending debt maturity as early as July 2024, they had ample time to adjust their positions ahead of the Q4 FY 2025 earnings announcement.

Calculating the Impact on Stock Price from Debt-to-Equity Conversion

Breaking down how one can quickly calculate debt‑to‑equity impact on share price:

In December 2024, MongoDB redeemed all of its 2026 Convertible Senior Notes by converting roughly $1.15 billion of debt into equity at a rate of 4.9260 shares per $1,000 principal.

1. Shares Issued

- Debt redeemed: $1.15 billion

- Conversion rate: 4.9260 shares per $1,000 debt

-

Shares issued:

1,150,000 units of $1,000 →

1,150,000 × 4.9260 ≈ 5,664,900 new shares

2. Share Count Before & After Conversion

- Pre‑conversion equity value: $1.61 billion

- Assumed pre‑conversion price: $280/share

-

Implied pre‑conversion shares:

1,610,000,000 ÷ 280 ≈ 5,750,000 shares -

Post‑conversion shares:

5,750,000 + 5,664,900 ≈ 11,414,900 shares (nearly double)

3. Theoretical Price Impact

Assuming a constant market capitalization:

New price = (Pre‑conversion market cap) ÷ (Post‑conversion shares)

= (5,750,000 × $280) ÷ 11,414,900 ≈ $141

In other words, dilution alone would cut the share price roughly in half—from $280 down to about $140.

4. Why the Stock Didn’t Fall That Far

- Dilution effect: Total shares nearly doubled, so value per share must adjust downward.

- Offsetting factors: Positive Q4 FY25 earnings, stronger balance‑sheet metrics and optimistic guidance prevented a full 50% drop.

- Actual range: Post‑earnings, MongoDB traded between $170–$190—indicating the market partially absorbed the dilution alongside improving fundamentals and investor sentiment.

Summary Table

| Metric | Value/Estimate |

|---|---|

| Debt converted | ~$1.15 billion |

| Shares issued for conversion | ~5.66 million shares |

| Pre‑conversion shares (approx.) | ~5.75 million shares |

| Post‑conversion shares (approx.) | ~11.41 million shares |

| Pre‑conversion price (approx.) | $280 |

| Theoretical post‑conversion price | ~$140 |

💡 By laying out the math clearly, readers can see how converting debt to equity drives dilution—and why the market only partially priced in that dilution when company results and outlook remained strong.

💡 A developing different investor thinking beyond headlines and applying a more independent analytic lens could have foreseen and navigated this outcome more effectively by adjusting position in January well ahead of market correction in Feb-April.

What we learned about MongoDB?

- Calculated Debt Conversion for Long‑Term Strength: MongoDB successfully converted debt into equity. Short term pain for shareholders, but long term gain for company and shareholders.

- Power of Financial Diligence: Investors who read into MongoDB’s debt levels and conversion terms had ample warning of the share‑price dip and could adjust their positions ahead of the “calculated fall.”

Is MongoDB investable?

After unpacking the debt‑to‑equity conversion and its market implications, here’s why I remain bullish on MongoDB (MDB):

- Debt‑Free Balance Sheet: With the $1.15 billion in 2026 notes fully redeemed, MongoDB unencumbered by debt and has increasing financial flexibility for innovation and expansion.

- Validated Growth: Two positive earnings reports since the restructuring underscore management’s ability to execute and drive sustainable cloud adoption. Guidance for FY 2025 and FY 2026 has been raised, reflecting confidence in continued top‑line momentum.

- Assets + Cash + Short Term Investments are all time high

- Liabilities + Debt are all time low

- Customer Adoption: MongoDB serves over 54,500 customers as of early 2025, with a strong presence among top tech and large enterprises- 70% of the Fortune 100 rely on MongoDB (this is huge green flag!).

- Revenue Growth: MongoDB’s subscription revenue is growing strongly (24% year over year for Atlas services), driven by both new customers and expanding adoption among existing clients.

- My Position: I initiated buy of MDB leap calls, and shares after the debt conversion was completed. My stake includes purchases in the $170–$200 range, giving me a strong cost basis and downside protection.

- Target Exit: I’m aiming for a $400/share sale by the end of 2026. Given ongoing margin expansion, broad enterprise adoption of Atlas, and the secular shift to cloud databases, this target feels well within reach.

💡 In a sector crowded with overvalued incumbents, MongoDB’s clean balance sheet, demonstrated execution, and clear runway for subscription‑driven revenue growth make it not just a compelling growth stock but also a safer bet in the face of a broader market correction.

Do the DD. Develop Different.

Disclaimer: This is not fiduciary advice. Please do your own due diligence and take full responsibility for your actions.